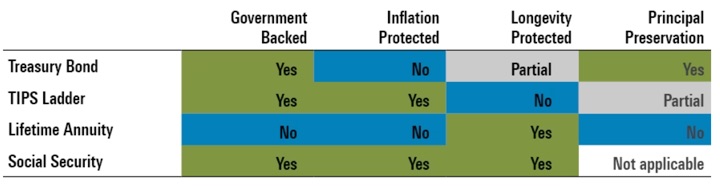

These days, when I see an article titled The Best Current Sources of Retirement Income, I expect to be pitched some sort of options-based ETF with 12% yield or high-yield junk bonds with a 9% yield. However, this Morningstar article actually provided a reasonable comparison of three high-quality options for “guaranteed” income:

- Traditional US Treasury Bonds, which offer a fixed interest payment for the remaining term of the bond (plus return of principal).

- Treasury Inflation Protected Securities (TIPS), which offer a variable interest payment that is a fixed amount above an inflation-linked index (plus return of principal).

- Single Premium Income Annuities, where you put up all your money upfront and then receive a fixed amount for the rest of your lifetime.

There are some additional assumptions, but here is a chart assuming a $100,000 investment, starting at age 65 with a 20-year time horizon that experiences 2.4% annual inflation (2.4% is the average long-term prediction of future inflation):

The chart seems to suggest that if you buy an annuity and then die the next year, you would lose your entire $100,000. That can be the case, but every SPIA annuity quote that I’ve seen offers the option to guarantee a certain minimum number of payments like 5 or 10 years of income, or a complete return of premium ($100,000 in this case). You do pay for this additional rider in the form of a lower monthly payout, but it is a popular option.

Don’t forget about Social Security. The article reminds us that an alternative option for government-guaranteed, inflation-adjusted income is to delay your Social Security start date and increase your future monthly payments for the rest of your life. Your cost is using your own funds to replace your income during those additional delayed years before claiming.

The results are about as you might expect, but it’s nice to see it illustrated using charts. My lightning recap:

- Moderate inflation (2.4%) + Average Lifespan: Mostly a tie.

- High inflation (5%) + Average Lifespan: TIPS win.

- Low inflation (1%) + Average Lifespan: Treasury bonds win.

- Moderate inflation + Extended Lifespan: SPIA lifetime annuity wins.

Since we don’t know the future, there is no “best” option. However, this comparison helps you understand why you’d own each option. If everything goes as forecasted, it won’t really matter what you pick. But I bother with owning all three types because I like knowing that I am covered in all of the more extreme scenarios. I don’t plan on buying a lot of private annuities, however, as Social Security is already an annuity that offers lifetime inflation-adjusted income. If needed, I plan to simply delay my Social Security claim date if I wish to increase my annuity allocation.